Trading on the 21 st Century Silk Road: Every millisecond counts

Republished from China Telecom Europe (China Market – Briefing).

By Edmund Cheung, Director of Marketing and Enterprise Business at China Telecom Europe & Devie Mohan, FinTech market expert and key industry influencer

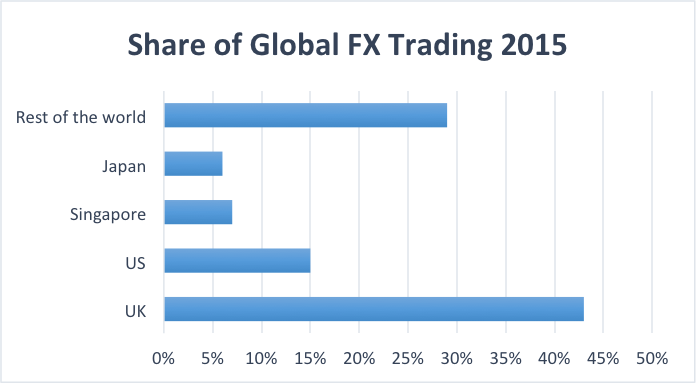

London is regarded as the world’s largest foreign exchange (FOREX) hub and handles over 40per cent of the global volume of around $5tn FOREX being traded each day. The capital is also the home of an offshore centre for renminbi (RMB) exchange and investment. Overall RMB trading volumes have more than doubled since 2013, up 143% with average daily volumes reaching $61.5bn. And that’s set to increase.

Source: TheCityUK

RMB will not only be used as a means of payment, but also an investment currency for companies to raise funds overseas. The UK was the first major western country to join the China-led Asian Infrastructure Investment Bank (AIIB). Along with expanding the use of RMB globally, this could enhance London’s role as the currency’s offshore centre.

This improved partnership between the UK and China has also contributed to the development of a number of several key relationships in the fintech sector. Several China-based start-ups have found investment in the UK and partnerships are being formed between entities on both sides, capitalising on the strength of each others’ markets.

So, what technologies should financial institutions take into consideration when trading with China and the Asia Pacific region (APAC)?

The need for speed

Today data can travel between the two countries in less than 150 milliseconds – that is faster than the blink of an eye. This low latency is crucial for traders in FOREX, and real-time trading markets such as capital, commodities and high frequency trading (HFT).

To maintain that edge, financial institutions should consider network providers who can offer reliable low latency connectivity, high bandwidth and redundancy tailored to meet the needs for time-sensitive markets. The telecommunications industry in China has invested over US$25 billion in their network infrastructure. Chinese network providers have intercontinental cables that connect the world’s major financial centres – from the US and Europe to APAC – with China. Financial institutions also need a network of high bandwidth point to point data services, known as International Ethernet Private Lines (IEPLs), for next generation Ethernet connectivity right across China.

Significant coverage

The number and locations of collocated data centres (DC) and Points of Presence (PoP) for nationwide coverage is key. To make the most of the growing Chinese market, a network provider must have solutions available across the entire country – from tier 1 to tier 4 cities – not just a few selected cities. A network provider must also have their Chinese PoPs collocated within the stock exchanges.

Timely and efficient innovation

One of the most important focus areas for financial institutions in the Asia-Pacific region is the achievement of superior, faster and more cost-efficient innovations. . China is playing an increasingly important role in the fintech industry; Chinese investment in innovation in Asia-Pacific firms has quadrupled, to hit a record high of $3.5bn in just the first nine months of 2015. China-based institutions have made significant investments in the Payments and Lending areas; two segments in particular have a direct interest in RMB value, with firms like Lufax and WeCash leading the race.

China’s market has displayed some unique fintech characteristics and trends that the internationalisation of the RMB will help develop further. For example, there are over 3,000 P2P lending start-ups in China, creating a total lending market of close to $15 billion. It also has a 38% unbanked population, but has also seen substantial growth in the penetration of fintech products and mobile banking. Significant interest from the international community in China’s currency and investments will propel this inward-facing market to massive growth externally, further increasing the opportunities in the payments and lending space.

With the increased internationalisation of RMB as a currency, innovation in areas like foreign exchange, currency transfer and invoicing can only grow. There will also be greater interest in the infrastructure and services around trading systems, exchanges and payments to support this increased interest.

Time as money

One issue that worries any trader is downtime. Each case of downtime can cost well over $500,000 an hour. That’s why financial institutions must have robust Service Level Agreements (SLAs) with their network providers. The SLA must contain latency commitments which details bandwidth and contingency guarantees.

As trade and investment between the UK and China move up a notch, London will play a key role as both the world’s FOREX hub and an offshore RMB centre. The old adage time is money rings true for the finance industry. Along with the need for speed, financial institutions also need a 24/7/365 network. Finally, the network provider must be more than just a purveyor of technology. It needs to be a partner who can provide insight and expertise into China’s regulatory framework and unlock the potential of this nascent and exciting financial market.